1. The Strategic Imperative of Machine Learning in Financial Security

Financial fraud is a colossal and ever-evolving threat, costing the global economy billions annually. For financial institutions and mobile payment services, the ability to rapidly and accurately detect fraudulent transactions is not just a matter of loss prevention, but a core component of maintaining customer trust and regulatory compliance. Traditional rule-based systems are often too rigid to keep pace with sophisticated criminal patterns, necessitating the adoption of advanced machine learning models.

This article details a complete, end-to-end data science project focused on developing a powerful, scalable, and deployable fraud detection system. The project moves systematically from initial data acquisition and deep exploratory analysis to robust model training using a custom pipeline, culminating in the creation of an interactive web application for real-time prediction using Streamlit. The foundation of this system is a comprehensive transaction dataset with millions of records, presenting the perfect challenge for addressing issues like class imbalance and feature engineering.

2. Deep Dive into Data Acquisition and Exploratory Analysis (EDA)

Effective fraud detection begins with a meticulous understanding of the raw data. The dataset utilized for this project, often sourced from large public repositories, is vast, containing over six million rows of transactional data. This scale requires powerful analytical tools and efficient processing techniques.

Dataset Structure and Initial Inspection

The raw dataset provides a detailed snapshot of mobile money transactions, capturing the history and state of both the sender and receiver accounts. Key columns include:

- Step: Represents a unit of time (e.g., hours or days).

- Type: The nature of the transaction (CASH_IN, CASH_OUT, DEBIT, PAYMENT, TRANSFER).

- Amount: The monetary value of the transaction.

- NameOrig / NameDest: The sending and receiving accounts.

- OldBalanceOrg / NewBalanceOrig: Account balances before and after the transaction for the sender.

- OldBalanceDest / NewBalanceDest: Account balances before and after the transaction for the receiver.

- IsFraud: The crucial target variable (1 for fraudulent, 0 for legitimate).

Initial analysis confirms that the data is remarkably clean, with zero missing (NA) values across all columns, streamlining the initial preparation phase. The shape of the dataset—approximately 6.36 million records across 11 columns—underscores the need for computationally efficient techniques.

Addressing the Class Imbalance Challenge

A defining characteristic of all real-world fraud detection problems is extreme class imbalance. The vast majority of transactions are legitimate. A simple count reveals only 8,213 fraudulent transactions compared to over 6.35 million non-fraudulent ones.

Calculated as a percentage, the fraud rate is approximately 0.13% of the total dataset.

If a machine learning model is trained on this skewed data without compensation, it can achieve a superficial accuracy of 99.87% simply by predicting “not fraud” for every single transaction. This deceptive high accuracy is useless. Handling class imbalance is therefore the single most critical step in building a viable fraud detection model, necessitating the use of specialized techniques like class weighting during model training.

Visualizing Transaction Patterns and Fraud Rates

To gain initial insights, data visualization is essential.

Transaction Type Distribution

A bar chart of transaction types reveals that CASH_OUT is the most frequent transaction, followed by PAYMENT and CASH_IN. DEBIT is the least frequent. This distribution immediately guides where to focus feature engineering efforts.

Fraud Rate by Type

Analyzing fraud rates across transaction types provides crucial strategic intelligence. The analysis shows that fraud is overwhelmingly concentrated in two types: TRANSFER and CASH_OUT. The fraud rates for CASH_IN, DEBIT, and PAYMENT transactions are negligibly close to zero. This empirical finding allows us to prioritize modeling efforts around the characteristics unique to Transfer and Cash Out transactions, which are often exploited by criminals to move funds quickly.

Analysis of Transaction Amount

Descriptive statistics for the Amount column reveal a wide range, from a minimum of zero to a maximum exceeding 92 million. The high standard deviation, relative to the mean of approximately $179,000$, confirms the presence of significant outliers. A log-scaled histogram helps visualize the true distribution of transaction amounts, highlighting that while most are small, the fraudulent activity is often associated with the highly varied, larger-end transactions. A box plot further demonstrates that the mean transaction amount for fraudulent activity, even when filtered under a threshold (e.g., $50,000), is significantly higher than for non-fraudulent activity.

3. Feature Engineering and Data Preparation for Modeling

Raw data rarely contains all the necessary signals for prediction. Feature engineering is the art of transforming raw variables into new features that better expose the underlying fraud patterns.

Creating Balance Difference Features

A key indicator of suspicious activity is an unexplained change in account balances. Two new features are created to capture this discrepancy for both the originator and destination accounts:

- BalanceDiffOrig: The difference between OldBalanceOrig and NewBalanceOrig.$$\text{BalanceDiffOrig} = \text{OldBalanceOrig} – \text{NewBalanceOrig}$$

- BalanceDiffDest: The difference between NewBalanceDest and OldBalanceDest.$$\text{BalanceDiffDest} = \text{NewBalanceDest} – \text{OldBalanceDest}$$

These features reveal discrepancies that may indicate accounts being deliberately emptied or manipulated. A quick check of the data shows a high number of instances where the BalanceDiffOrig is negative, suggesting accounts that have money removed without a corresponding logical update, a common sign of transactional anomaly.

Identifying High-Risk Account Behavior

Further feature analysis focuses on account patterns known to be exploited by fraudsters: accounts being emptied after a transfer. A boolean filter is created to identify records where an originator account had a positive balance before the transaction and zero balance immediately afterward, specifically for TRANSFER and CASH_OUT types. This filter exposes over a million highly suspicious records that warrant closer investigation and could serve as a powerful engineered feature.

Dimensionality Reduction and Correlation Analysis

Before modeling, the relationships between numerical features are assessed using a correlation matrix. Visualized as a Seaborn heatmap, the matrix reveals:

- High Internal Correlation: A near-perfect correlation (0.98) exists between

NewBalanceDestandOldBalanceDest, which is expected but highlights some data redundancy. - Moderate Fraud Signal:

Amountshows a moderate positive correlation (around 0.46) withNewBalanceDest, suggesting that larger transactions significantly impact the receiver’s balance, a signal that may be leveraged by the model.

Feature Selection and Data Splitting

For the final model, several columns are dropped to eliminate noise or redundancy:

- NameOrig and NameDest: These categorical columns, while unique, are too high-cardinality to be practically useful in a linear model without excessive complexity.

- IsFlaggedFraud: This is a secondary regulatory flag and not the primary target variable.

The final features are split into:

- Categorical:

Type(Transaction Type). - Numerical:

Amount,OldBalanceOrig,NewBalanceOrig,OldBalanceDest,NewBalanceDest,BalanceDiffOrig,BalanceDiffDest.

The data is then partitioned into training (70%) and testing (30%) sets using the train_test_split function, ensuring stratification on the target variable (IsFraud) to maintain the true proportion of fraud cases in both sets.

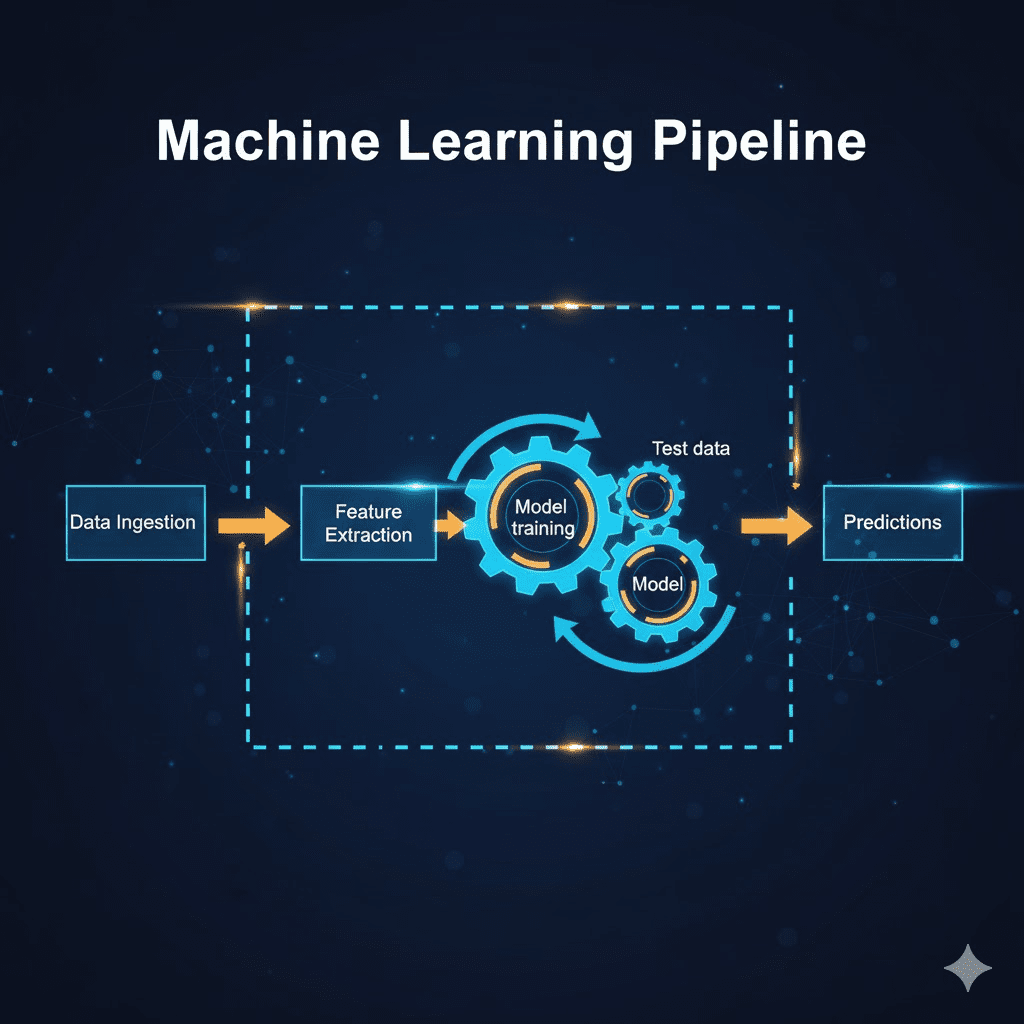

4. Constructing the Machine Learning Pipeline and Evaluation

A robust data science solution is not just the model itself, but the entire processing workflow encapsulated into a single, reliable unit. The Scikit-learn Pipeline is the ideal tool for this, combining data preprocessing and model training into one object that can be seamlessly trained, evaluated, and exported.

The Preprocessing and Model Pipeline

The pipeline is constructed using the ColumnTransformer to apply specific transformations to different data types:

- Numerical Features: Scaled using a StandardScaler to normalize the range of values (important due to the large difference in the

Amountcolumn), preventing features with larger absolute values from dominating the learning process. - Categorical Features: Converted into a machine-readable format using OneHotEncoder with the

drop='first'option to prevent multicollinearity.

The final pipeline chains the ColumnTransformer with the classifier: Logistic Regression.

Crucially, the LogisticRegression model is initialized with class\_weight='balanced'. This is the core solution for the class imbalance problem. By assigning a higher penalty (weight) to misclassifying the minority class (fraud), the model is forced to prioritize catching the rare fraudulent transactions, rather than achieving high overall accuracy by defaulting to “not fraud.” The maximum iterations are set to 1000 to ensure convergence on the large dataset.

Training, Prediction, and Model Evaluation

The pipeline is trained on the stratified training data (X_train, Y_train). Upon completion, predictions are generated on the held-out test set (X_test). The model’s performance is then evaluated using metrics that look beyond simple accuracy:

- Accuracy: The model achieves a score of approximately 99.94%. While high, this must be viewed in context.

- Classification Report: This provides a clearer picture of the model’s true effectiveness, focusing on the minority class:

- Recall (Fraud Class): This is the fraction of actual fraud cases that the model correctly identified. A high recall is paramount in fraud detection to minimize costly false negatives (missed fraud).

- Precision (Fraud Class): This is the fraction of predicted fraud cases that were actually fraudulent. Lower precision means more false positives (flagging legitimate transactions as fraud), which can harm customer experience.

- Confusion Matrix: This visualizes the counts of True Positives, True Negatives, False Positives, and False Negatives, allowing for a precise understanding of the model’s trade-offs.

The final model demonstrates a strong capability in detecting fraudulent transactions, achieving a high recall rate on the minority class due to the class weighting, making it a viable candidate for deployment.

5. Model Deployment: Creating an Interactive Streamlit Web Application

The final step in any data science project is deployment, making the predictive power accessible to end-users. For rapid prototyping and internal tools, Streamlit is an excellent choice, allowing the creation of a powerful web application purely in Python.

Exporting and Loading the Pipeline

The fully trained and evaluated pipeline object is exported using the Joblib library. This process serializes the entire workflow—including the scalers, the one-hot encoder logic, and the trained logistic regression model—into a single file (e.g., fraud\_detection\_pipeline.pickle). This file is then loaded into the Streamlit application, ensuring the live prediction environment uses the exact same preprocessing steps as the training environment.

The Streamlit Application Structure

The web application provides a simple, intuitive user interface for real-time risk assessment:

- Interface Setup: The app is given a clear title and instructions, and a visual divider is used for clean segmentation.

- User Input Fields: Intuitive input fields are created for the user to enter the transaction details:

- Transaction Type: A

st.selectboxfor the categorical input (Payment, Transfer, Cash Out, etc.). - Amount, Balances: Multiple

st.number\_inputfields collect the sender’s old/new balances and the receiver’s old/new balances.

- Transaction Type: A

- Data Structuring: When the “Predict” button is clicked, all user inputs are immediately collected and formatted into a Pandas DataFrame that perfectly mirrors the structure of the data used for training. This step is critical for ensuring the exported pipeline can process the inputs without error.

- Prediction and Output: The structured input DataFrame is passed to the loaded pipeline’s

.predict()method. The result (0 or 1) is captured. - User Feedback: The prediction is immediately presented to the user with clear visual feedback:

- Success Message: If the prediction is 0 (not fraud), an

st.successmessage confirms the transaction looks legitimate. - Error Message: If the prediction is 1 (fraud), an

st.errormessage warns that the transaction can be fraud.

- Success Message: If the prediction is 0 (not fraud), an

This deployed application enables risk analysts to assess suspicious transactions manually by inputting the details and instantly receiving a model-driven risk assessment. For additional resources on developing and deploying Streamlit applications, this guide provides excellent starting points for deployment best practices.

Conclusion

The successful creation and deployment of this machine learning-based fraud detection system underscore the immense value of a comprehensive, structured data science methodology. Starting with a massive, imbalanced dataset, the project demonstrated the necessity of rigorous exploratory data analysis, the creation of highly relevant engineered features (like balance differences), and the strategic application of class weighting to overcome the critical challenge of class imbalance. Encapsulating this entire process within a Scikit-learn Pipeline ensured operational consistency, while deploying the final model via a Streamlit web application delivered the analytical power into a practical, real-time assessment tool. This framework provides a scalable blueprint for organizations seeking to augment their financial security measures with the precision and speed of artificial intelligence.