In a world where digital innovation shapes the future of finance, a powerful new framework is acting as the catalyst for a new era in global payments. This framework is Open Banking, a transformative protocol that is fundamentally rewiring the relationship between banks, businesses, and consumers. It promises a future that is more interconnected, secure, and personalized than ever before. But what exactly is open banking, and how is it poised to disrupt decades-old financial systems?

At its core, open banking is a regulatory and technological protocol that allows for the secure sharing of financial data between traditional banks and authorized third-party service providers (TPPs). This sharing is facilitated through the use of Application Programming Interfaces (APIs). Under this model, consumers and businesses can grant explicit consent to regulated FinTech companies, allowing them to access specific bank account details. This empowerment enables those authorized companies to build a new generation of financial services, such as real-time account-to-account (A2A) bank transfers, sophisticated budgeting tools, and streamlined lending applications.

The term “Open Banking” gained significant prominence with the introduction of the European Union’s landmark payments regulation, the Payment Services Directive 2 (PSD2). This directive effectively mandated that banks in the EU create secure APIs to allow customer-permissioned access, a move designed to spur competition and innovation in the financial sector. For most consumers, the most visible impact of this regulation is a new payment method at checkout, often labeled “Pay by Bank Transfer” or “Pay by Bank.”

The adoption of this model has been explosive. In the United Kingdom alone, the number of open banking users surpassed 8 million in 2023. This is not a niche trend; it is a fundamental market shift. Globally, open banking transactions are projected to skyrocket, with some forecasts predicting a total value of over $330 billion by 2037. For merchants, financial institutions, and everyday users, understanding this revolution is no longer optional.

The Engine of Open Banking: How APIs Create a Secure Bridge

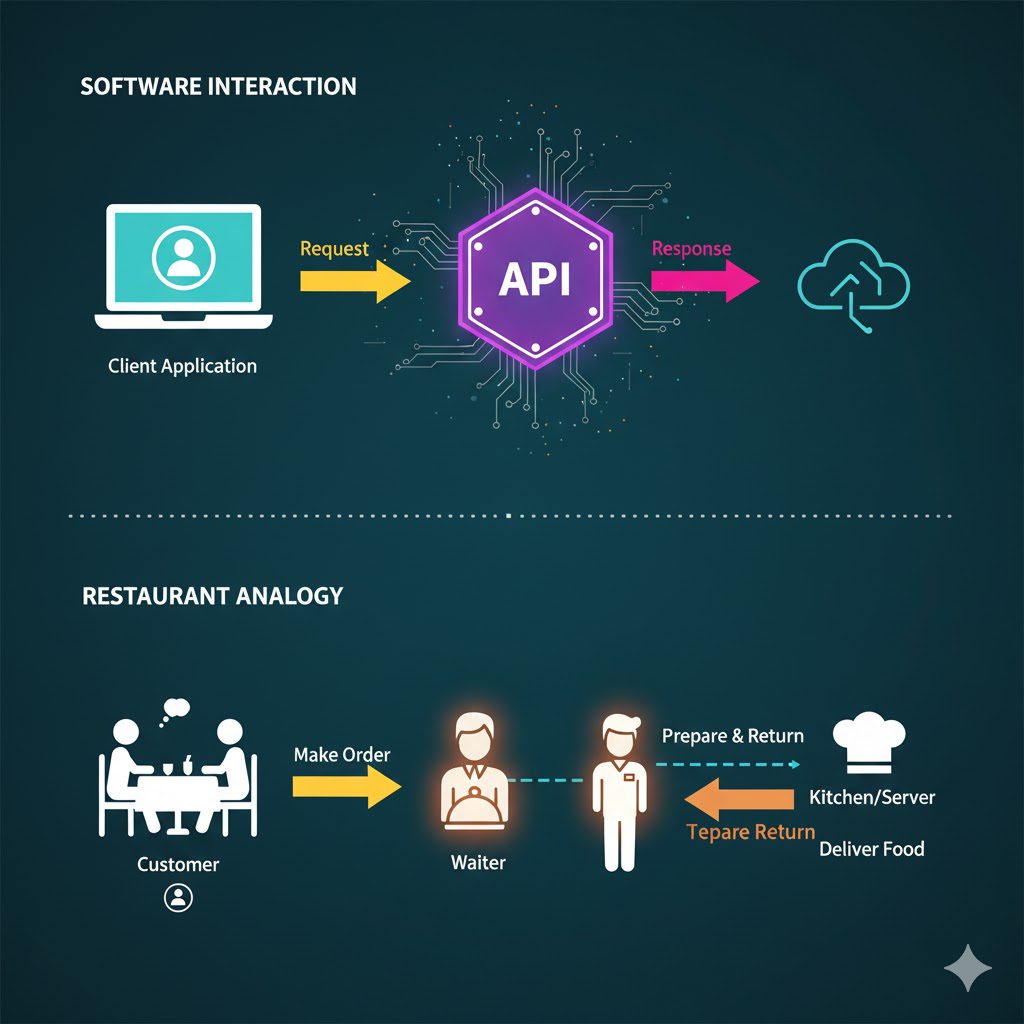

Before diving into the benefits, it’s crucial to understand the core technology that makes open banking possible: the API. An Application Programming Interface is a set of rules and protocols that allows different software applications to communicate with each other. In the context of open banking, an API acts as a secure messenger or a digital handshake.

Think of your bank account as a secure vault. In the past, the only way to access that vault was to use the bank’s own key (your debit card) or go directly to the bank’s website (your online banking login). Open banking, through APIs, creates a new, highly secure “service entrance” to that vault.

When you use a FinTech app to check all your bank balances in one place, you give that app permission to access your data. The app then sends a secure, encrypted request via the bank’s API to the bank’s server. The bank’s server, after verifying the request and your consent, sends back only the specific, read-only data that was requested—such as your account balance and transaction history. At no point does the third-party app ever see or store your banking login credentials.

These aren’t the public APIs that developers might use to build a weather app. These are highly regulated, private APIs built with bank-grade security, heavy encryption, and strict access tokens. This technology is the foundational bedrock upon which the entire open banking ecosystem is built, providing a standardized way for data to be shared safely and efficiently, all under the complete control of the account holder.

Why Merchants are Championing the “Pay by Bank” Revolution

For decades, the online checkout process has been dominated by credit and debit cards. While familiar, this system is fraught with friction, high costs, and security risks. Open banking payments, or Account-to-Account (A2A) transfers, offer a powerful alternative that directly addresses these pain points, which is why merchants are eagerly adopting this new payment rail.

1. A Radically Improved Checkout Experience

The traditional checkout is a conversion killer. Customers are forced to manually find their wallet, type in a 16-digit card number, expiry date, and CVV code, and often a billing address. This process is tedious, error-prone, and a major source of “cart abandonment.”

Open banking eliminates this friction entirely. When a customer selects “Pay by Bank Transfer,” they do not manually enter any payment details. They are simply redirected to their own, highly trusted mobile banking app or online banking portal to approve the pre-filled payment request. This process, which leverages biometric authentication (face or fingerprint) on their phone, reduces the time to complete a transaction from minutes to mere seconds. For merchants, a faster, simpler checkout directly translates to higher conversion rates and fewer abandoned carts.

2. Sky-High Acceptance Rates

A hidden drain on e-commerce revenue is the high rate of declined card payments. Transactions can fail for a multitude of reasons: an expired card, an incorrect CVV, a mistyped digit, or an overzealous fraud-detection system at the card-issuing bank.

Open banking transactions, by contrast, boast success rates of over 95%. This reliability stems from the payment’s direct nature. The payment is a “push” transaction initiated directly from the customer’s bank account, which has already been authenticated. The system checks the balance in real-time, and if the funds are available, the payment is confirmed. There are no card network intermediaries, no CVV numbers to mistype, and no expiry dates to worry about. For merchants, this means more approved transactions and more predictable revenue.

3. A Bank-Grade Fortress Against Fraud

Fraud is a multi-billion dollar problem for online merchants. Open banking is, by design, one of the most secure payment methods available today, thanks in large part to its compliance with PSD2’s Strong Customer Authentication (SCA) requirement.

SCA mandates that a customer must complete a two-factor authentication process to initiate a payment. This typically involves a combination of two of the following:

- Knowledge: Something only the user knows (e.g., their banking password or PIN).

- Possession: Something only the user has (e.g., their mobile phone, verified by a one-time passcode).

- Inherence: Something the user is (e.g., their fingerprint or face scan).

When a customer pays with open banking, they are redirected to their own secure banking environment to authenticate. This means the merchant never handles or sees any sensitive payment credentials. The bank, which has the most robust security, manages the entire authentication process. The combination of secure APIs and bank-level SCA creates a dual defense against fraudsters, making it an exceptionally secure way for customers to pay.

4. The End of the Chargeback Headache

For any business selling online, the word “chargeback” is a source of immense frustration. A chargeback is a forced reversal of a card transaction, typically initiated when a customer disputes a charge with their card issuer. While a vital consumer protection tool, this system is often abused, leading to lost revenue, administrative burdens, and additional chargeback-related fees for the merchant.

Open banking payments essentially mitigate this risk. Because the transaction is a real-time bank transfer authenticated and “pushed” by the customer directly from their account, the concept of a chargeback as it exists in the card world does not apply. The payment is considered final and irrevocable, similar to a wire transfer. This provides merchants with payment finality and protects them from this significant source of revenue loss.

5. Faster Access to Cash Flow and Instant Payouts

In the traditional card model, it can take days, or even a week, for a merchant to receive the funds from a customer’s purchase. This lag in settlement ties up working capital.

Open banking operates on real-time (or near-real-time) payment rails. When a customer approves the payment, the funds are transferred from their bank to the merchant’s bank almost instantly. This same real-time infrastructure also applies to payouts and refunds. If a customer needs a refund, the merchant can send the money back to their account immediately, dramatically improving the customer experience. For the merchant, this faster access to funds optimizes cash flow and simplifies financial planning.

The Customer Revolution: More Than Just a Payment Button

While the merchant benefits are clear, open banking is equally, if not more, revolutionary for consumers. The ability to securely share data (with explicit consent) has unleashed a wave of innovation in personal finance.

A Unified View of Your Financial Life

Gone are the days of logging into five different apps and websites to check your checking account, credit card, savings, and loans. Open banking empowers FinTech companies to create financial dashboards and budgeting apps. These tools can, with your permission, pull in read-only data from all your different financial accounts and present them in one unified, easy-to-understand interface. You can track your spending, analyze your habits, and see your entire net worth at a glance, giving you unprecedented control over your financial health.

Access to Better, Faster Financial Products

This new data-sharing capability is also transforming how consumers access credit and other financial products. Traditionally, applying for a loan or mortgage involved manually gathering months of paper bank statements, pay stubs, and tax documents—a slow and arduous process.

With open banking, you can grant a lender temporary, secure access to your transaction history. The lender’s algorithm can then analyze your actual income and spending habits in minutes, not days. This leads to fairer and more accurate underwriting decisions, faster loan approvals, and the ability to get personalized quotes for products like insurance based on your real-world financial behavior, not just a generic credit score.

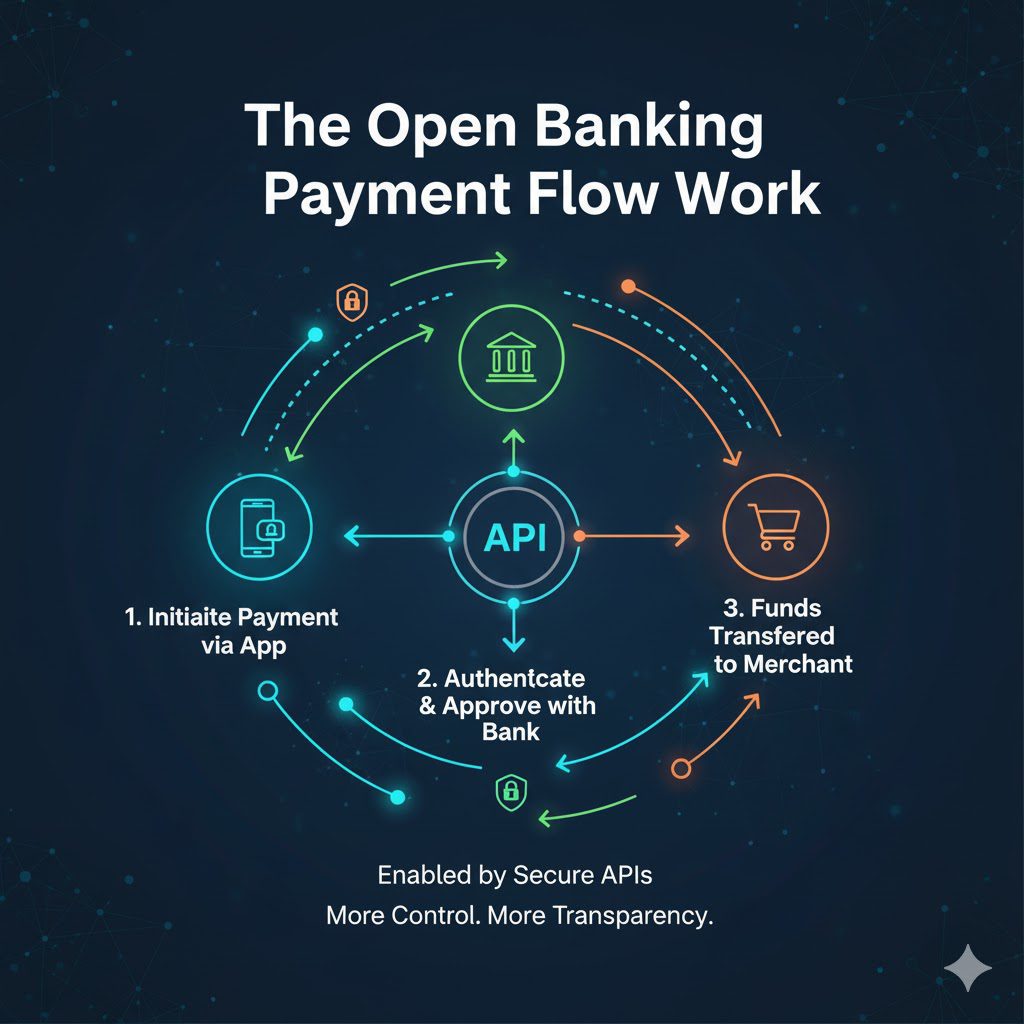

How Open Banking Payments Work: A Simple, Secure Journey

For the end-user, the open banking payment process is a masterclass in secure simplicity. While the underlying technology is complex, the customer-facing experience is designed to be seamless and build trust.

- Select at Checkout: The customer shops on a website and proceeds to the payment page. Alongside credit cards and digital wallets, they select the “Pay by Bank Transfer” (or similarly named) option.

- Choose Your Bank: The customer is directed to a secure page where they see a list of banks. They select their own bank from this list.

- Secure Redirect: This is the most critical step. The customer is instantly and securely redirected to their own familiar online banking environment (either the mobile app on their phone or the bank’s official website). The merchant is never part of this interaction.

- Authenticate and Confirm: Inside their secure bank portal, the customer sees all the payment details pre-filled: the merchant’s name and the exact amount. They simply authenticate the payment using their standard, trusted method—be it their fingerprint, face, or banking password.

- Payment Complete: Once authenticated, the payment is instantly confirmed. The customer is redirected back to the merchant’s website with a “payment successful” message.

The Road Ahead: Challenges and the Dawn of “Open Finance”

Despite its immense momentum, the open banking journey is not without its challenges. Widespread adoption requires overcoming hurdles in data privacy, standardization, and public awareness. Consumers are rightfully cautious about their financial data, and the industry must constantly reinforce the “consent-driven” nature of the model, battling “consent fatigue” and ensuring users fully understand what they are sharing.

Furthermore, the global landscape is fragmented. While the EU and UK have a regulatory-driven approach (PSD2), other markets like the United States have a more market-driven system, leading to different standards and speeds of adoption.

However, the future is already expanding beyond just banking. The next logical evolution is “Open Finance”. This applies the same principles of data sharing and APIs to a much wider range of financial products, including:

- Pensions and Investments: Securely sharing your investment portfolio data with a financial advisor or planning tool.

- Mortgages: Simplifying the application and management of home loans.

- Insurance: Allowing apps to compare your current insurance policies and find better deals.

This “Open Finance” model promises a truly holistic, 360-degree view of an individual’s entire financial life, powering even more personalized and automated services.

Conclusion: From Closed Walls to an Open Financial Horizon

Open banking is not merely a new payment method; it is a fundamental paradigm shift. It represents the move from a closed, siloed, and product-centric financial industry to one that is open, interconnected, and resolutely consumer-centric. By placing control over financial data firmly in the hands of the consumer, it has unlocked a wave of innovation that is creating tangible value for all stakeholders.

For merchants, it offers a lifeline: a way to cut costs, dramatically reduce fraud, and eliminate the friction that kills conversions. For consumers, it is the key to a new world of financial control, convenience, and access to better products. While the road to full global adoption is still being paved, the foundation is set. The future of finance is open, and it is poised to create a more efficient, secure, and empowered global economy.